Fixing ERCOT

The Texas electrical grid has become a leader in renewables and batteries. But there are storms on the horizon and the grid operator ERCOT as well as Texas needs to start thinking long term.

ERCOT stands for the Electric Reliability Council of Texas, and their job is to run the grid within Texas. Now ERCOT doesn’t cover all of Texas, but it does cover the majority of it. ERCOT is unique among all the electricity markets in the US as it is a deregulated real time energy market. Other markets use capacity planning to determine what they need, but not ERCOT. Developers can build what they want and all ERCOT does is act as the market clearing house, seeing that consumers get charged and producers get paid based on the constantly changing price of electricity.

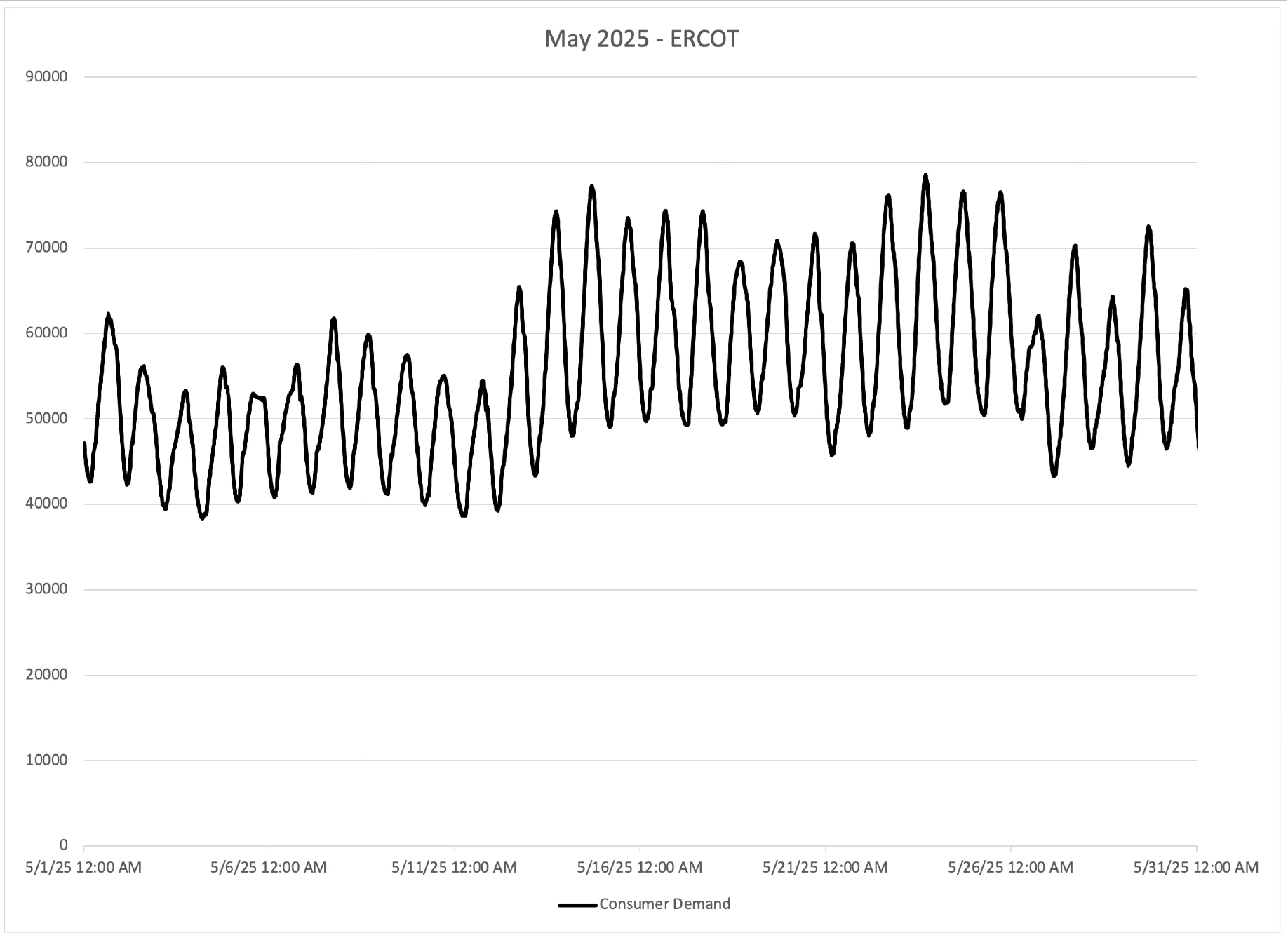

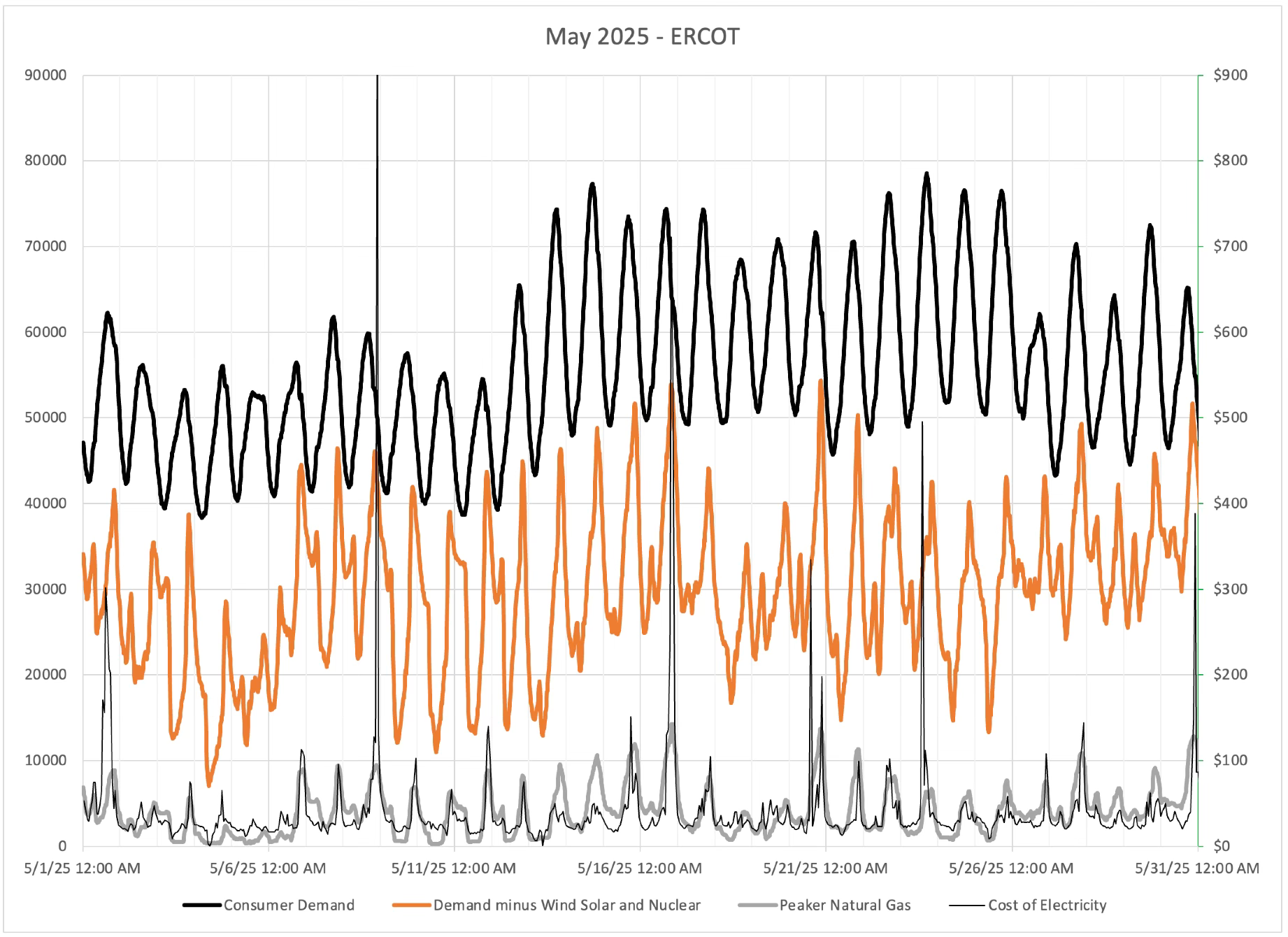

So this was the demand curve for ERCOT during May 2025 showing how many megawatts of electricity where being delivered every fifteen minutes through the month. The swing from 5 am in the morning to 5 pm in the evening can be almost 30,000 megawatts of electricity. But, developers within ERCOT have added a lot of solar lately as it is the cheapest and most profitable. And that solar has reduced those 5 pm demand highs which used to be the major worry for ERCOT ten years ago.

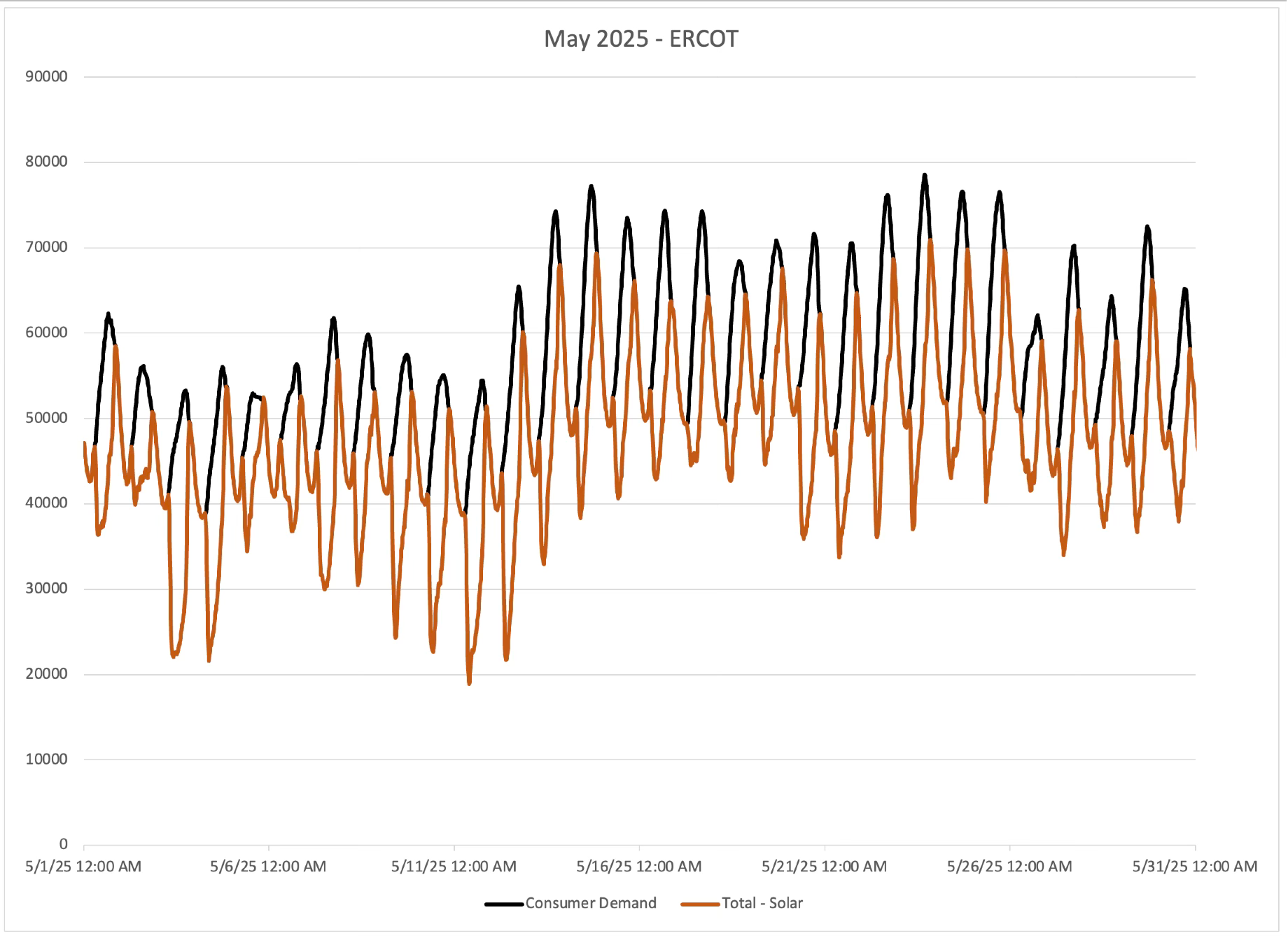

Once you subtract the solar power from the consumer demand, you end up with the orange line above. The peaks have dropped down, but now they have become a spike in demand at 8pm in the evening and at 7 am in the morning. And those spikes are quite sharp. This is the new worry for ERCOT. Not the heat of the day, but rather the loss of solar in the evening.

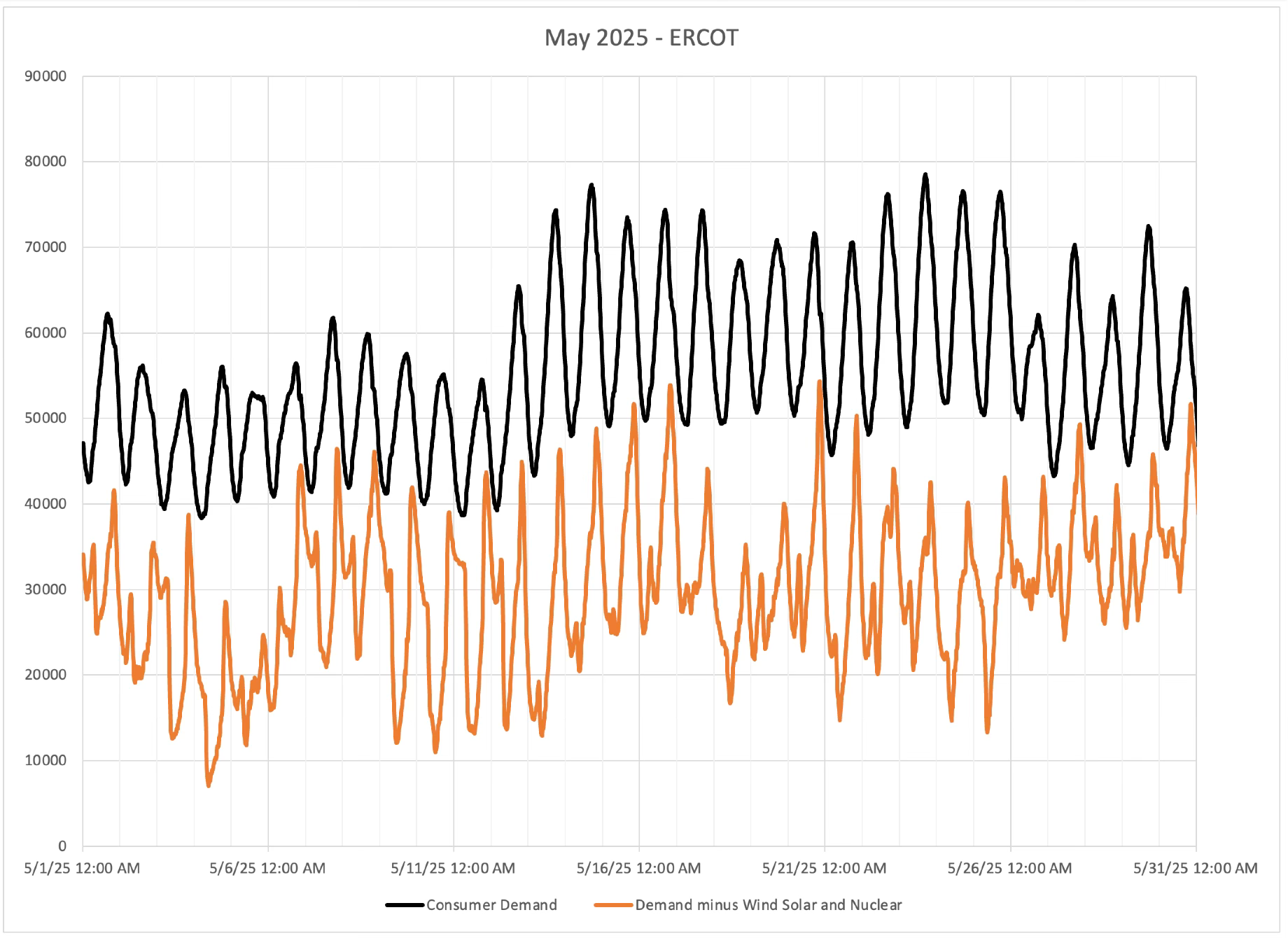

And it gets even worse when you account for the power generated by wind and nuclear. This orange line above is what all the rest of ERCOT has to supply. Natural gas and coal have to generate power to meet the orange line and as a result they have to change output a lot.

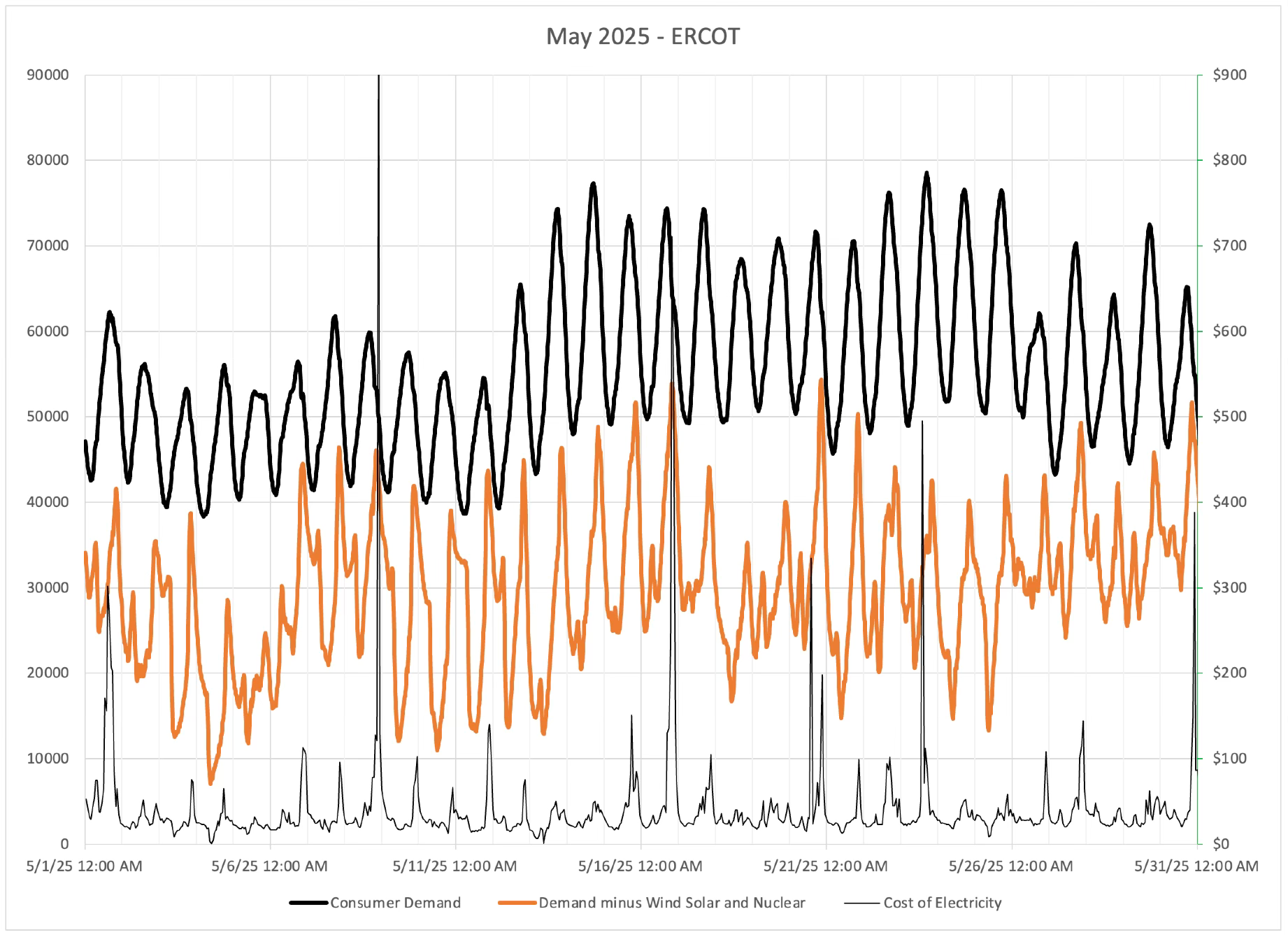

And we see that reflected in the cost of electricity. The wholesale cost of electricity fluctuates and spikes during those same power demand spikes. The 6pm to 10pm window has become the time when the highest electricity prices occur. As the sun sets and solar goes to zero and before the nightly winds pick up, we get a high demand on natural gas and coal, and we see high pricing as a result.

And it is specifically the natural gas peaker power plants that are the cause of those high prices. Peaker power plants are natural gas engines that drive generators. They can start quickly and supply power for a short time and then shut down when not needed. But as they have a low utilization factor, they charge hundreds of dollars per megawatt-hour for the short time that they run. They are also less efficient and need 50% more natural gas per megawatt-hour to produce electricity than their more efficient cousins - the natural gas combined cycle power plants.

Batteries have also become a new player in the short term power supply. But while we have over 8,000 megawatts of battery capacity, they only store about 12,000 megawatt-hours. When over the course of a day natural gas peaker power plants supply over 100,000 megawatt-hours.

What this means is that the Texas ERCOT grid, and really all of America’s major electrical grids are dependent on natural gas as the swing fuel. The fuel that adjusts to changing consumer demand and changing renewables. But, the problem is that puts more pressure on the natural gas supply. A supply that is facing a doubling of natural gas exports via the lignified natural gas export terminals that are springing up.

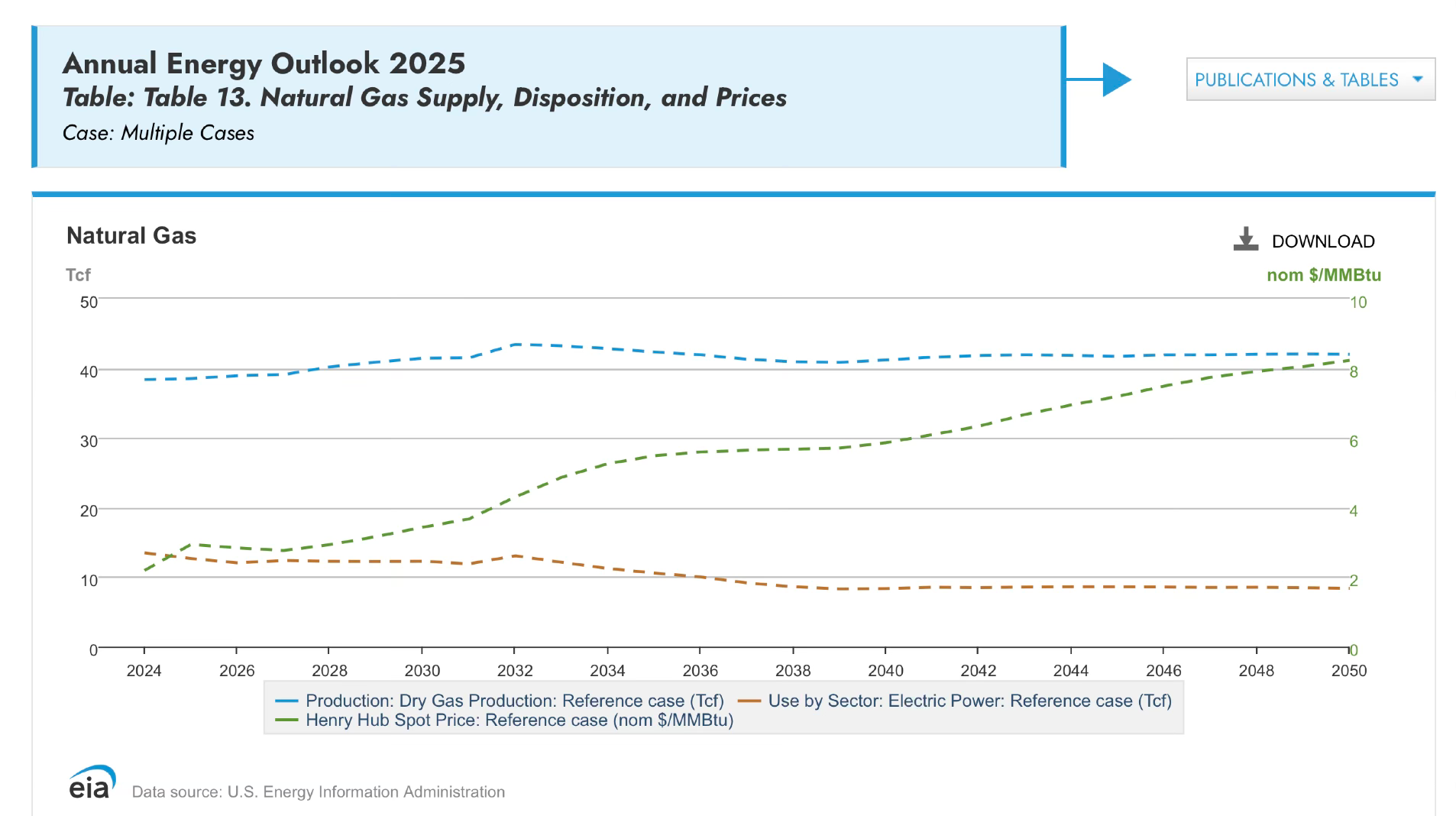

The Energy Information Agency (EIA) of the Department of Energy publishes an Annual Energy Outlook that comes out every two years. The last report was published in April 2025 and it shows a natural gas supply that is slowly increasing and then staying fairly constant through 2050.

But it also shows electric power plants using less natural gas. And that directly relates to the green line on the graph - an increasing natural gas price. Hidden within the report are predictions of increased natural gas exports and with a fairly constant production rate, that can only come from higher prices causing consumers and electric power plants to use less natural gas. This prediction flies in the face of the increasing data center power demands that have the market for natural gas turbine generators totally overloaded. If you wanted a brand new peaker natural gas power plant you would need to order it now and delivery is going to be sometime in 2031 - six years out.

The volatility of the electric markets is causing a lot of data centers to look for dedicated power suppliers. The most outlandish being that Microsoft is looking at restarting the Three Mile Island nuclear power plant to power a data center. But, the far more common solution is to locate natural gas peakers at the data center to provide that dedicated power.

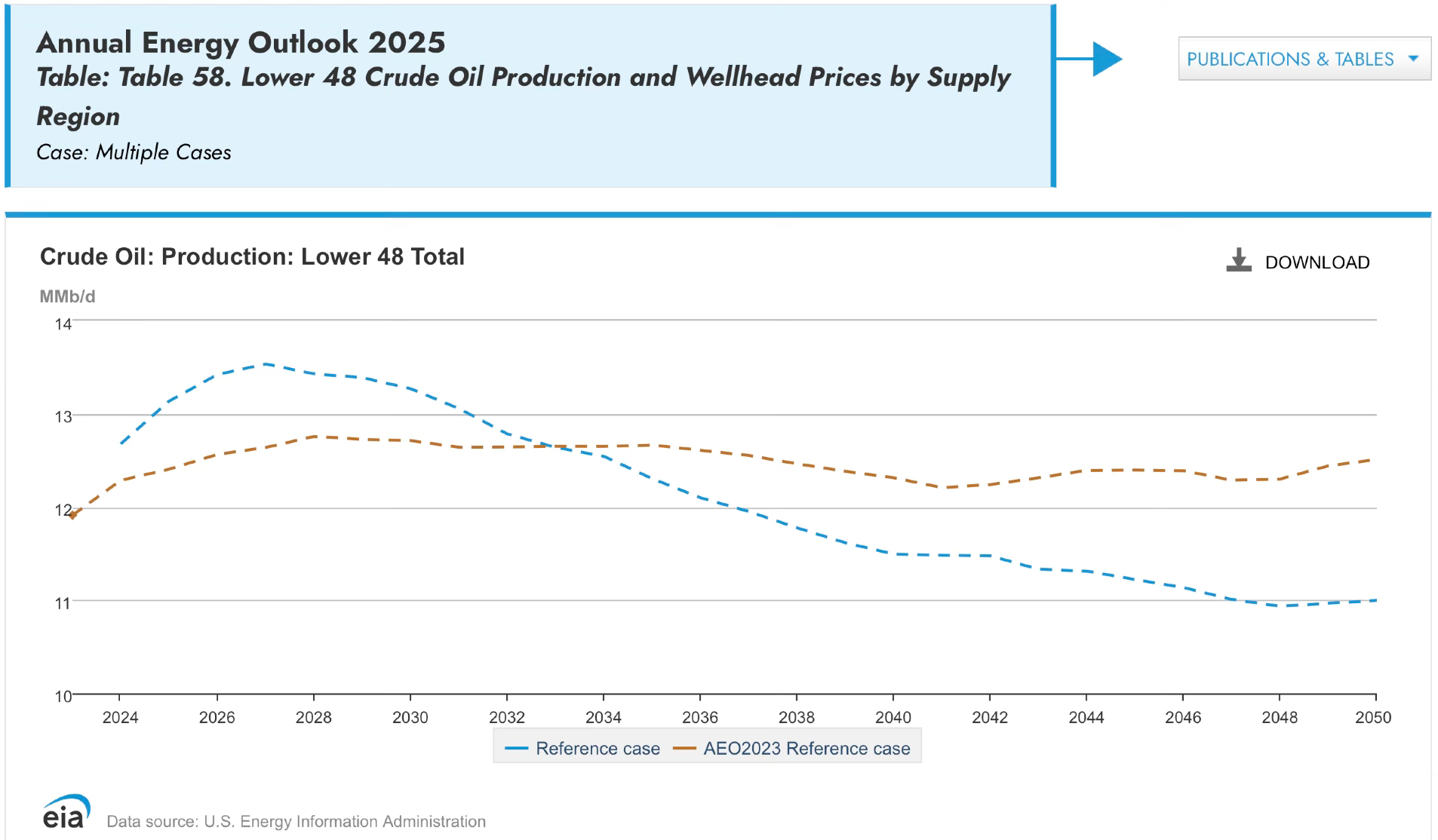

My view is that EIA is behind the times with their natural gas predictions. And that should not come as a big surprise, as they made a big change on their predictions for the US domestic oil production market.

The orange line is the 2023 prediction and it showed fairly stable production for the next twenty-five years, much like this year’s gas production. So, what changed this year to make EIA (2025 blue line) predict a peak in 2026 followed by a pretty serious decline? Predictions from industry experts and oil company CEOs that US domestic oil production was about to peak. These predictions have been coming hot and heavy for the last five years and this April, EIA finally produced a report that listens to them.

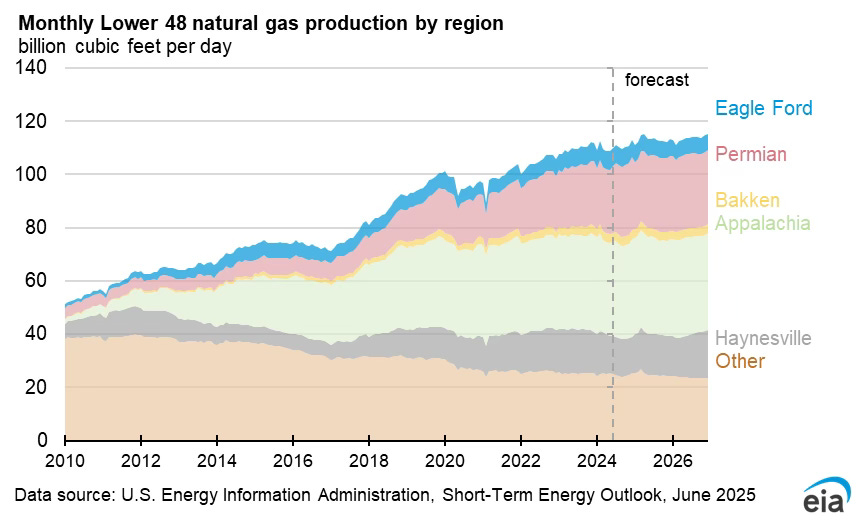

My concern is that we have the same possibility with natural gas. Especially since the only natural gas field to increase its output last year was the oil-dominated production from the Permian, and with the Permian peaking that is going to stop. There are some analysts claiming that production from the Haynesville and other natural gas shale fields will increase. But if it does happen it will be a short term event. The United States has more than doubled its domestic production since 2010. To do that we have drilled the best gas acreage in the shale fields and there is just no way we can keep that level of production going for the next ten years. The natural gas shale fields have all been showing slowing production plateauing as more and more of their drilling is going to replace the declining production from older wells.

What about coal? Trump is now proclaiming he will bring back coal. There are some fundamental problems with coal. First you get less energy per pound from coal than natural gas and you get a lot more pollutants from coal. Natural gas burns cleanly and produces half the carbon dioxide that coal does.

Want “clean coal”? That involves carbon capture which means it takes 45% more coal to make the same megawatt-hour of electricity. We may be forced to turn to coal in the short term, but it isn’t a long term solution.

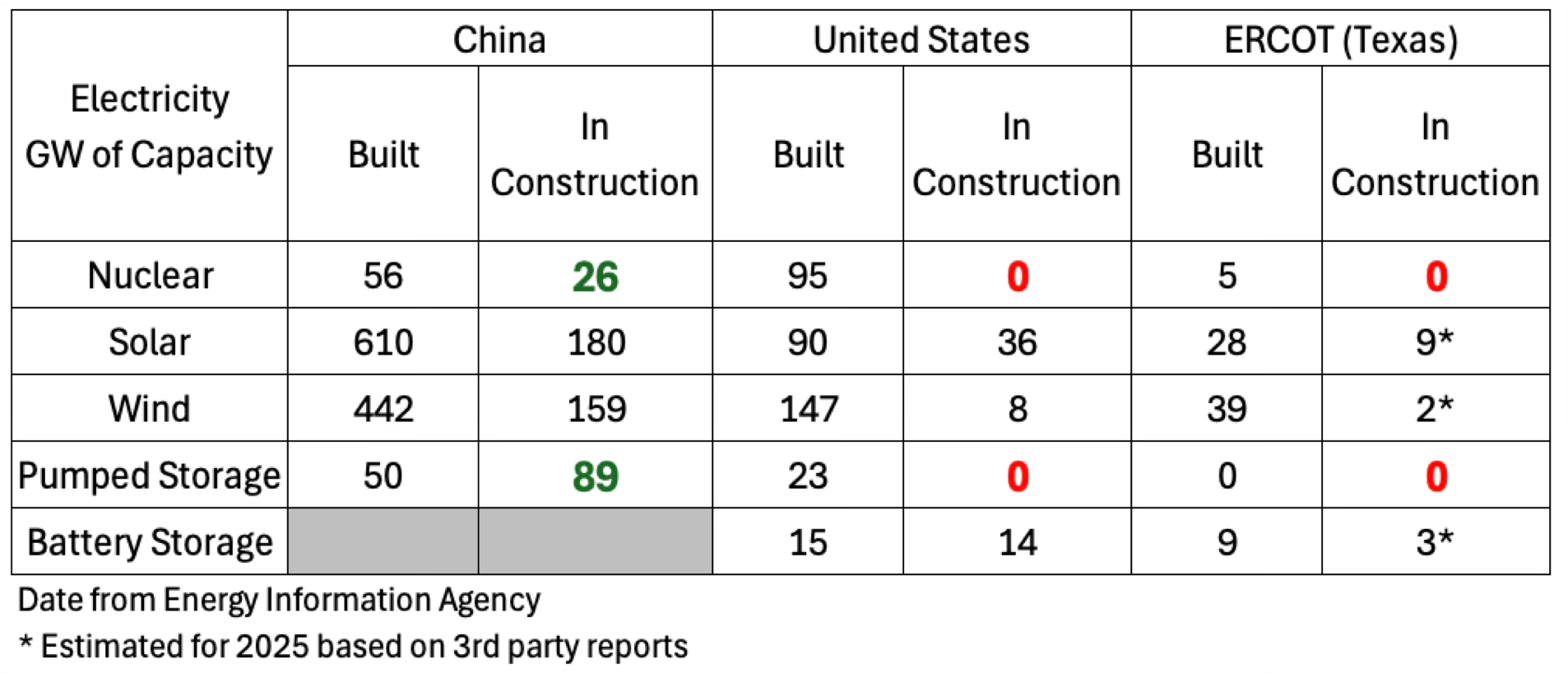

Interestingly enough we can learn from our geo-political rival China. People make a lot of noise about China building coal power plants, but what they fail to realize is how much China is building of renewables, nuclear, and most importantly long duration energy storage.

China has taken a longer view and is building a lot of nuclear and pumped storage hydroelectric - the oldest and most reliable form of long duration energy storage (LDES).

LDES is batteries, but a battery that can store lots of energy. Enough for it to power the grid for over ten hours. Unlike most grid lithium ion batteries which are one to two hours. And that longer storage means that LDES acts like giant shock absorbers helping to stabilize the grid.

And this is where Texas’s goes wrong. The ERCOT market is set up to treat batteries and LDES like any other power producers on the grid. They only get paid for the market price of the electricity that they supply. There are some ancillary services that can be earned, but the lithium-ion batteries have that market locked up. So, new batteries and LDES are only making money based on arbitrage - the difference between the price they pay to charge up and the higher price when they put the electricity back on the grid. And that means they need volatility, those massive swings in electricity prices are what gets the batteries paid.

In 2022 and 2023, the volatility was high and battery operators made a lot of money. That was the price signal for them to add a lot more batteries to the ERCOT grid pushing us up to the over 8,000 megawatts we have now. But in 2024, a cooler summer combined with lower natural gas prices (and therefore cheaper peaker power plant electricity) meant that battery operators found themselves not getting the same prices they did in the years before.

That decreased volatile revenue and the threat of the loss of Federal funding for battery incentives combined with tariffs has led to the cancellation of a number of projects. The Houston Chronicle reported that 4,000 megawatts of battery projects had been cancelled in 2025.

The truth is that the addition of LDES and batteries reduces the volatility and makes for a more stable market price, thereby reducing the arbitrage. So, if the addition of batteries means the price is better for consumers, but the batteries get paid less, no developer in the world is going to build more batteries, let along LDES. We need to change the market mechanism to supply a stable, bankable, value for energy storage the developers can count on.

And that is what ERCOT needs to do. To stop thinking of batteries and LDES like power generators, but think about them as a means of moving power in time, from periods of excess cheap power to when power is needed. Just as transmission lines move power from where it is generated to where it is needed, batteries move power from when it is in excess to when it is needed.

The solution is simple, transmission lines are paid for by the whole grid through a service charge. Energy storage needs to receive a service charge from the renewables whose variability is what they are solving for. The answer is a small fee taken from every megawatt-hour that wind and solar puts on the grid that would go into a fund. That fund would then pay a service charge for every megawatt-hour that energy storage put onto the grid. The energy storage provider would get the arbitrage as well as the storage payment, which would encourage the most efficient storage providers. The solar and wind fee would start out low and rise as more storage was added to the grid. But that additional storage would also allow more solar and wind to be added without disrupting the grid. The additional storage would act as a shock absorber keeping the power prices more constant and increasing the reliability of the electrical grid.

The Department of Energy has modeled what a future grid with a much higher percentage of renewables looks like and long-duration energy storage was absolutely critical to making that future grid work. But the only way LDES is going to get built in Texas is if there is a stable market mechanism that rewards the LDES developers and is something that gives banks the confidence to loan money to build LDES.

The other solution is for the Texas Legislature to adjust the law around the Texas Energy Fund. The fund was created to supply loans to natural gas power plants to be built in Texas. A number of the projects that applied for the fund have withdrawn as natural gas turbine deliveries have gotten longer and projects have become uneconomic in light of increasing gas prices. It is time for the fund to be opened up to long duration energy storage and nuclear power plants. These and more solar are going to be needed in the future and it is time for the Texas Legislature, the Texas Public Utilities Commission, and ERCOT to start taking a longer view.